$1 Million Life Insurance Policy- Best Rates By Age

One of the most common questions I receive is what is the cost of a one million life insurance policy? The good news is that the best rates on a one million life dollar insurance policy can be very affordable and have favorable underwriting guidelines if you choose the right company. If you’re looking for a million dollar life insurance policy cost comparison for the best rates with favorable underwriting, then this article is for you.

The reality is that there are over 700 life insurance companies in the United States and each one will have their own price for a ten million dollar life insurance policy. Factors such as age, health, medications, and many other aspects will determine your premium. The key is to compare rates from the top companies to see which insurer will offer the best rate for your specific age and health. Whether it is Prudential, AIG, Mutual of Omaha, Pacific Life, Banner Life, Protective Life, Principal, Symetra Life, Lincoln Financial or another carrier, comparing rates from many of the nation’s top carriers before you move forward is paramount if you want the best rate and most favorable underwriting to get approved at that rate. Many people are incredibly surprised to see how much the rate can differentiate from one life insurance company to the next.

Table of contents

- How to get a one million life insurance policy

- Underwriting a million life insurance policy

- $1 million life insurance policy – exam vs. no exam vs. accelerated underwriting

- $1,000,000 life insurance underwriting guidelines by age and company

- Common health conditions that affect a $1 million life insurance policy

- $1 million term life insurance policy cost

- Sample Rates for $1 million 20 year term life insurance policy

- $1 million whole life insurance policy cost

- $1 million ($1,000,000) life insurance policy-wrap up

- FAQ

How to get a one million life insurance policy

Quotes

The first step is to receive quotes from multiple companies to compare rates for the best price. You can call the different insurance companies yourself or have an independent broker shop the market for you. (There is no charge for a broker, the same price you receive from an agent-broker is the same price as going to the company directly.

Select a company and start the application

Choose the best company and complete the application.

Paramed (if it’s fully underwritten), phone interview if it’s a no exam policy

Schedule and complete the 30-minute no-cost paramed exam. If it’s a no-exam policy, complete the phone interview.

Underwriting process

Wait for the underwriting process to be completed. Your age and health will help determine how long it will take. The underwriter may request your medical records, which they will obtain.

Approval

Once approved, you will receive the policy, review it, and if you accept then make the first payment. You don’t have pay anything until you are approved and accept the policy, unless you want coverage during the underwriting process. The policy will go inforce and the coverage is active.

Underwriting a million life insurance policy

Each life insurance company has their own underwriting guidelines and niches for a million dollar life insurance policy, the rates can vary significantly. For example, Prudential Life Insurance Company has great underwriting guidelines in many areas including for people who chew or use dip. They are one of only a few companies in the country that offer a non-tobacco rate which will be about half the price of the other life insurance companies. Another example is with a top life insurance company called Banner Life. They are great for people with diabetes and can typically provide a more favorable health class then the other top companies and in return offer a much lower premium. These are just a few examples, since each company has their own price and niche. That is why it is imperative to call the top companies to receive multiple quotes or use a broker who can do the shopping for you to ensure you are receiving the best rate for specifically for you and your age, health, family history, etc.

$1 million life insurance policy– exam vs. no exam vs. accelerated underwriting

Many people prefer to avoid a medical exam if they can, especially over this past year with COVID-19. While life insurance underwriting has come a long way in the decade, it is still not perfect. There are a few companies that you can obtain a one million life insurance policy with no paramed exam at all and the rates are competitive to those with the exam. Then there are other companies that offer a one million life insurance policy with no medical exam policy at all as well but the rates are very expensive, sometimes double that of those with an exam. The next option is something called accelerated underwriting (AU).

Accelerated underwriting typically involves a phone interview to see if you qualify for the no exam policy and goes up to $1 million in coverage. This type of policy is for people in good health as about 50% of applicants qualify for accelerated underwriting. If you qualify for accelerated underwriting the approval is faster and doesn’t require the paramed. Also, the carriers that offer this are some of the most well-known and best life insurance companies in the country.

If you do try to get approved for the accelerated underwriting policy and the after the phone interview, the underwriter requests the paramed exam, it’s not the biggest deal, as you would have had to take the 30 minute no-cost paramed anyway and you are still with one of the best companies in the country.

Whether you choose a policy with the exam, or no exam or the accelerated underwriting, all three will look at the prescription database, check the MIB (Medical Information Bureau) and look at your driving history.

No exam and accelerated underwriting polices are typically for those between the ages of 18 to 60 years old.

For more information and options available for a one million dollar no-exam term life insurance policy view our article $1 million no-exam term life insurance rates.

$1,000,000 life insurance underwriting guidelines by age and company

So exactly what are the underwriting requirements to be approved for a ten million life insurance policy? Below are the exact requirements from a few of the nation’s top life insurance companies to provide an example of exactly what they look for when underwriting a one million dollar life insurance policy.

Prudential (Pruco) Life Insurance Company

18 to 40 years old- Paramed, (Possible AU), IRP, MVR report

41-45 years old- Paramed, (Possible AU), ECG, IRP

46-50 years old- Paramed, (Possible AU), ECG, IRP

51-64 years old- Paramed, (Possible AU to age 60) ECG, IRP

65- 70 years old- Paramed, ECG, IRP

71-75 years old- Paramed, APS, IRP, COG, FRAILTY, MOBILITY, Rx

Over 75 years old- Paramed, APS, IRP, COG, FRAILTY, MOBILITY, Rx, MVR

Definitions

Paramed- paramed exam- which includes height, weight, blood pressure and a small blood and urine sample

MVR- Motor Vehicle Report (driving record)

IRP- Insurance risk profile (comprehensive blood and urine panel)

ECG- Electrocardiogram- (same as EKG), examiner brings out the machine when does the paramed

APS- Attending Physician Statement (medical records)

COG- Cognitive functioning test, administrated by the examiner

FRAILTY- Senior supplement questionnaire, administrated by the examiner

MOBILTY- Get Up & Go mobility test, administrated by the examiner

Rx- Pharmaceutical database check

AIG- American General Life Insurance Company

40-44 years old- Paramed, BU, MVR, CR

45-49 years old- Paramed, BU, MVR, CR

50- 55 years old- Paramed, BU, MVR, CR

56- 59 years old- Paramed, BU, MVR, CR

60- 66 years old- Paramed, BU, MVR, CR

67-70 years old- Paramed, BU, MVR, FQ, CR, AC

71+ years old- Paramed, BU, MVR, FQ, ES, CR, AC, EKG, 71IR

Definitions

Paramed- paramed exam- which includes: height, weight, blood pressure, pulse

BU- Full blood profile and urine analysis

MVR- Motor vehicle report

FQ- Financial Questionnaire

ES- Electronic records search

TT- Tax Transcript

CR- Credit Report

TPF- Third party financial provided by CPA

AC- Agent Certification form

EKG-Resting electrocardiogram

IRP- Expanded Inspection Report which includes, Cognitive Tests. This test takes about fifteen minutes.

Pacific Life Insurance Company

41-50 years old- Paramed, HOS, Blood, (Possible AU, no exam, no blood, APS)

51-60 years old- Paramed, HOS, Blood, (Possible AU, no exam, no blood, APS)

61-70 years old- Paramed, HOS, Blood/NT-ProBNP, APS, IR (age 65+), (Possible AU, no exam, no blood, APS)

71 years old and over- Paramed, HOS, Blood/NT-ProBNP, APS, IR, FCA

Definitions

Paramed- paramedical exam-height, weight, blood pressure

APS- Attending Physician Statement (medical records)

BLOOD- Blood Profile

FCA- Functional Cognitive Assessment

HOS- Home Office Specimen (Urine Sample)

IR- Inspection Report

NT-ProBNP- Natriuretic Peptide Test (link to article on Pro-BNP)

Common health conditions that affect a $1 million life insurance policy

As mentioned earlier, each carrier will have their own price for for a one million life insurance policy. The key is to know which company will offer the best rate for your situation. Whether it be your age, build, any medications, family history, driving record, etc. Below are some common health conditions that can significantly affect which life insurance company will offer the best rate.

Build- height & weight

-Cholesterol readings- total, HDL, triglycerides

-Blood pressure readings

-Diabetes- pre-diabetes, type II, type I, gestational diabetes history

-Family history

-Stents

-Heart attack

-Asthma

-Alcoholism

-Driving record

-Calcium Score

-Elevated PSA

-Pacemaker

-Arthritis- osteo and rheumatoid

-TIA (mini-stroke)

-Stroke

-Cerebral Aneurysm

-Barrett’s Esophagus

-Ulcerative Colitis

-Crohn’s Disease

-Heat Valve

-Bypass

-Sleep Apnea

-ADD & ADHD

-DVT- Deep Vain Thrombosis

-SVT- Supraventricular tachycardia

-Tachycardia

-Atrial Fibrillation (A-fib)

-Marijuana

-Cancer history- prostate, melanoma, thyroid, breast, family, other

-Elevated Liver Functions

-Elevated Pro-Bnp

-Elevated microalbumin ratio

-Elevated GGT

-Elevated calcium score

-Elevated serum creatine

-Abnormal EKG

-Depression, one or multiple medications

-Anxiety, one or multiple medications

-Opioid use

-Cigar users

-Chew/dip users

-MS- multiple sclerosis

Other factors:

-Aviation

-Certain Avocations

-Scuba Diving

-Foreign travel to certain countries

-Bankruptcy or multiple bankruptcies

The are many more but these are some of the most common. Since each company does underwrite these health conditions differently, it’s important to compare rates from several companies.

$1 million term life insurance policy cost

Below are the best rates for a $1,000,000 term life insurance policy, male at the preferred plus health class.

| Age | 10 Year Term | 15 Year Term | 20 Year Term | 25 Year Term | 30 Year Term | |

| Age 40 | $26 month | $33 month | $49 month | $76 month | $92 month | |

| Age 45 | $44 month | $64 month | $85 month | $120 month | $146 month | |

| Age 50 | $69 month | $100 month | $129 month | $200 month | $240 month | |

| Age 55 | $121 month | $161 month | $217 month | $356 month | $453 month | |

| Age 60 | $206 month | $277 month | $381 month | $682 month | NA | |

| Age 65 | $355 month | $474 month | $738 month | $1,275 month | NA | |

| Age 70 | $589 month | $920 month | $1,518 month | NA | NA | |

| Age 75 | $1,195 month | $2,308 month | NA | NA | NA |

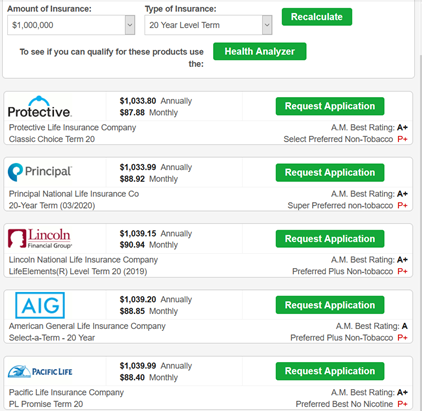

Sample Rates for $1 million 20 year term life insurance policy

$1 million whole life insurance policy cost

Below are the rates for a $1,000,000 million guarantee universal life insurance policy (no-lapse guarantee) for a male to age 121 years old at the preferred plus health class.

| Age | Premium |

|---|---|

| 35 | $379 month |

| 40 | $478 month |

| 45 | $582 month |

| 50 | $742 month |

| 55 | $952 month |

| 60 | $1,250 month |

| 65 | $1,682 month |

| 70 | $2,410 month |

| 75 | $3,342 month |

| 80 | $5,343 month |

$1 million ($1,000,000) life insurance policy-wrap up

Securing a one million dollar ($1,000,000) life insurance policy at the best rate can be easy if you know where to go and how to choose the right company. There are literally hundreds of life insurance companies in America and each one will offer a different rate based on several factors. Your age, height and weight, medications, your readings (blood pressure, cholesterol, liver enzymes, etc.), and many other aspects will determine which insurance company will have the lowest rates for you. This is why it’s imperative to compare rates from multiple carriers with a high financial rating to ensure that you are receiving the best rate and with a great company.

FAQ

Is $1 million of life insurance expensive?

The cost for a $1 million life insurance policy will depend on several factors including your age, health, build and how long you would like the policy for. Rates are as low as $26 month for a healthy 40-year old for a 10-year level term up to $1,094 a month for a 70-year old in average health.

Is $1 million of life insurance enough?

A rule of thumb is to have about 10x your annual income in life insurance coverage. This would replace your income for ten years if you were to pass away. Everyone has a different financial situation and need but this is a general rule of thumb.

Do I qualify for $1 million in life insurance?

Qualifying for a $1 million life insurance policy will depend on your gross annual income, age and how much life insurance you current have in place, outside of your employer. Many carriers will allow you to go up to 30x your annual income in total life insurance (excluding group coverage from work) for those between the ages of 20-40, 20x gross annual income for ages 41-50, 10x gross income for ages 61-70 and 5x income for those 70-80 years old.

Keep Reading

- $750,000 No Exam Life Insurance

- $1 Million No Exam Life Insurance

- $2 Million No Exam Life Insurance

- 5 Million Dollar Life Insurance Policy

- 10 Million Dollar Life Insurance Policy Cost

- Life Insurance Company Ratings 2024

- Pacific Life Insurance Review

- AIG Life Insurance Review

- 10 vs 15 vs 20 vs 25 vs 30 Year Term

- 35 Year Term Life Insurance Policy

- 9 Best No-Lapse Guarantee Universal Life (GUL) Insurance Companies

*Rates updated 3/14/2024