Banner Life Insurance Review 2024 (Ultimate Guide)

last updated on March 25, 2024

last updated on March 25, 2024Banner Life Insurance Company Overview

| Banner Life | By The Numbers |

|---|---|

| Financial Rating | A+ (Superior) |

| Comdex Score | 95 |

| Founded | 1836 (Legal & General) |

| BBB Rating | A+ |

| Customers | 1.5 million |

| Term Life Coverage Issued Annually | $63 billion |

| Claims Paid Annually | $1 billion |

| Industry Rankings | Ranked #1 provider of term life insurance in America |

| Term Lengths Available | 10, 15, 20, 25, 30, 35 or 40 years |

| No Exam and Lab Free | Majority of applicants qualify |

Banner Life Insurance Company based in Fredrick, Maryland and a subsidy of Legal & General America is ranked the number one provider of term life insurance in America. Banner Life is one of the oldest, largest, highest rated and best life insurance companies in America that you probably never heard of.

Since Banner don’t spend money much on traditional television adverting like many other large life insurance companies, this allows them to pass the savings on to their customers and often will have the lowest term life insurance rates in the entire country for many niches: healthy people, those with diabetes, those with a cancer history, those with health issues and are table rated for build (height/weight) and many other underwriting categories.

In our Banner Life Insurance Review 2024, we we go over everything you need to know about Banner Life to make an informed decision on whether or not they will the best choice as your term life insurance company.

Banner Life Is One Of Our Favorite Go To Companies- Here’s Why!

Best Rate Class- Preferred Plus Eligible For:

- Cigarette smokers 3 years out (quit)

- Clients with treated and controlled Hypertension (High Blood Pressure)

- Clients with treated and controlled high cholesterol

- Clients with a combination of treated high blood pressure and/cholesterol

- Clients with treated or untreated total cholesterol under 300

- Clients who participate in recreational scuba diving up to 100 feet

- Clients with a family history of cancer which is not due to a hereditary cancer syndrome

Preferred Health Class Eligible For:

- Clients with Asthma on two medications or less (well controlled)

- Clients with Anxiety/Depression on one prescription medication (well controlled)

- Clients with mild Sleep Apnea (Apnea Index (AI) <20 or Respiratory Disturbance Index (RDI) < 30 and lowest oxygen saturation above 85% with good compliance for one year and no residual symptoms

Standard Plus Health Class Eligible For:

- Clients with controlled Type II Diabetes (A1c 6.9 or less)

- Clients with Severe Sleep Apnea with documented good CPAP compliance for one year and no residual symptoms

- Clients with personal history of cancer, subject to type, date of onset and treatment including efficacy

Aviation

Preferred Plus rate class may be available for pilots of major airlines flying in the US and Canada without any other aviation exposure.Preferred Plus and Preferred rate classes may be available with an Aviation Exclusion Rider for other aviation activity.

Cigar smokers

Occasional cigar users and not other forms of tobacco are eligible for the best health class if:

- the use is admitted at the time of application/inquiry and all case data coincides with the admitted degree of usage,

- no more than one cigar per month; and

- no nicotine metabolites (cotinine) are present in the urinalysis done within the past 12 months; and

- there is no use of tobacco products other than occasional cigars for at least 3 years prior to the time of application or inquiry

Non-Tobacco (Non-Smoker) User Classification

In order to receive a non-tobacco rate with Banner Life you need to meet these qualifications:

- Not one cigarette in the past 12 months

- no more than one cigar per month

- no nicotine (cotinine) present in the urinalysis done within the past 12 months

- there is no use of tobacco products other than occasional cigars for at least 3 years prior to the time of application or inquiry

Marijuana use

- May qualify for non-tobacco rates as of 2024.

Recreational Scuba Diving

Preferred Plus rates available if:

- Dives do not exceed 100 feet

- PADI, NAUI, or SSI certified and all dives are done with dive master or instructor

- open water dives only

- does not participate in wreck, salvage, ice or cave diving

- no personal history of disease or impairment that would adversely affect mortality

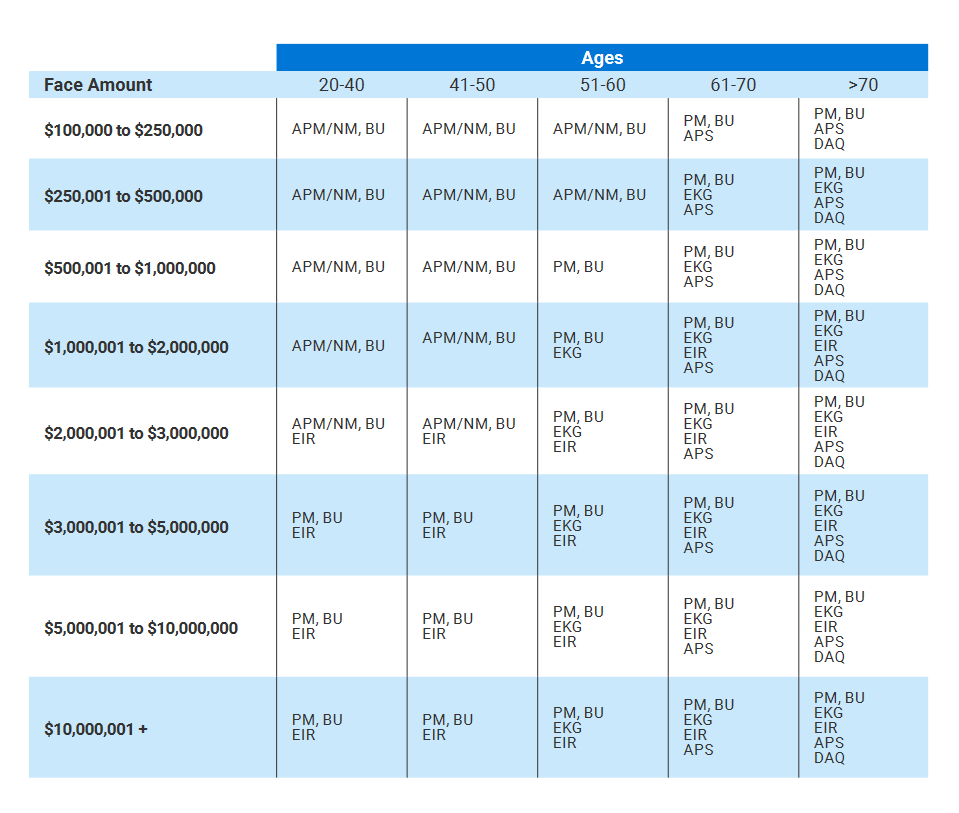

Banner Life Insurance Underwriting Requirements By Age Chart–From $100k to $10 Million +

How Long Is The Banner Life Insurance Paramed Exam Good For?

| Ages- 20 to 60 | Ages 61- 80 | Ages over 80 |

|---|---|---|

| 12 months | 6 months | 3 months |

Banner Life Insurance Additional Life Insurance Underwriting– Key Points

Preferred Plus May Be Available:

- Anxiety/Depression/Mood Disorder – One episode, duration of less than one year, recovered, no current medication

- Asthma – Mild exercise induced asthma or mild seasonal asthma

- Carotid Imaging – CIMT mildly increased for age/gender, no plaque or carotid stenosis.

- Echocardiogram – mild diastolic dysfunction, echocardiogram otherwise normal, BP well controlled.

- Mitral Valve Prolapse – Mitral valve normal appearing with normal thickness and echocardiogram otherwise normal, no regurgitation

- Osteoporosis – No known complications

- Skin cancers – Basal cell carcinoma, and superficial squamous cell carcinoma. Single atypical nevus or dysplastic nevus: no history of melanoma or family history of melanoma, with well documented and favorable dermatology follow up.

Preferred health class may be possible even with the following conditions:

- Alcohol or Single Drug Abuse Treatment – Last used more than 10 years ago, single episode of treatment, without any relapse, total abstinence from any mood-altering drug and no subsequent alcohol or drug related issues.

- Anxiety/Depression/Mood Disorder – Current, on one drug, well controlled.

- Dysplastic Nevi – Up to 3 atypical or dysplastic nevi with no history of melanoma or family history of melanoma, with well documented and favorable dermatology follow-up care.

- Valvular Disease – One valve mildly thickened or redundant valve, no mitral valve prolapse, less than mild regurgitation, rest of echocardiogram normal.

Banner Life Insurance Preferred Plus Health Classes Underwriting Guidelines Chart

Preferred Plus (Non-Tobacco)

Aviation: Available with exclusion rider.

Avocation: Available, if no flat extra premium would be required.

Blood Pressure: Currently well controlled with or without

treatment, with the average readings

in the past two years not greater than

135/85.

Cancer History: Only available for certain types of skin cancer.

Cholesterol: 120-300, with or without treatment.

Chol/HDL Ratio: May not exceed 4.5 with or without

treatment.

Driving History: No more than 2 moving violations in

last 3 years. No DWI, DUI, reckless/negligent driving,

license revocation or suspension in the last 5 years.

Family History: No cardiovascular death in either parent or siblings prior to age 60 more than

one parent before age 60.

CAD-coronary artery disease is disregarded for applicants over

age 70 who don’t use tobacco.

Impairments: No personal history of disease or impairments that would affect mortality.

Residency/Citizenship: U.S. citizen or legal permanent resident

/green card residing in the U.S. at least 3 years.

Substance/Alcohol Abuse: No abuse history.

Tobacco Use: No use of tobacco or nicotine-based

products in last 36 months. One cigar

allowed per month with negative urine specimen

for cotinine.

Banner Life Insurance Preferred Plus Health Classes Underwriting Guidelines Chart

Preferred (Non-Tobacco/Tobacco)

Avocation: Available, however may have a flat

extra.

Blood Pressure: Currently well controlled with or without

treatment, with the average readings

in the past two years not greater than

140/90.

Cancer History: Only available for certain types of skin cancer.

Cholesterol: 120-300, with or without treatment.

Chol/HDL Ratio: May not exceed 5.5 with or without

treatment.

Driving History: No more than 2 moving violations in

last 3 years. No DWI, DUI, reckless/negligent driving,

license revocation or suspension in the last 5 years.

Family History: No cardiovascular death of more than

one parent before age 60.

CAD-coronary artery disease is disregarded for applicants over

age 70 who don’t use tobacco.

Impairments: Can have personal history of certain

diseases or impairments.

Residency/Citizenship: U.S. citizen or legal permanent resident

/green card residing in the U.S. at least 3 years.

Substance/Alcohol Abuse: No abuse in past 10 years.

Tobacco Use: No use of tobacco or nicotine-based

products in last 24 months. One cigar

allowed per month with negative specimen for cotinine.

Banner Life Insurance Health Class Standard Plus Underwriting Guidelines Chart

Standard Plus (Non-Tobacco)

Aviation: Available, however may have flat extra

or exclusion rider. Private pilots over

age 70 require an aviation exclusion

rider.

Avocation: Available, however may have a flat

extra.

Blood Pressure: Currently well controlled with or without

treatment, with the average readings

in the past two years not greater than

145/90.

Cancer History: Available depending on type and date

of onset of cancer.

Cholesterol: 120-300, with or without treatment.

Chol/HDL Ratio: May not exceed 6.5 with or without

treatment.

Driving History: No more than 3 moving violations in

last 3 years. No DWI, DUI, reckless/negligent driving,

license revocation or suspension in the last 3 years.

Family History: No cardiovascular death of more than

one parent before age 60.

CAD-coronary artery disease is disregarded for applicants over

age 70 who don’t use tobacco.

Impairments: Can have personal history of certain

diseases or impairments.

Residency/Citizenship: U.S. citizen or legal permanent resident

/green card residing in the U.S. at least 2 years.

Substance/Alcohol Abuse: No abuse in past 7 years.

Tobacco Use: No use of tobacco or nicotine-based

products in last 12 months. One cigar

allowed per month with HO specimen

negative for cotinine

Banner Life Insurance Health Class Standard Underwriting Guidelines Chart

Standard (Non-Tobacco/Tobacco)

Aviation: Available,however may have flat extra

or exclusion rider. Private pilots over

age 70 require an aviation exclusion

rider.

Avocation: Available, however may have a flat

extra.

Blood Pressure: Currently well controlled with or without

treatment, with the average readings in the past two years not greater than

156/94.

Cancer History: Available depending on type and date

of onset of cancer.

Cholesterol: 120-300, with or without treatment.

Chol/HDL Ratio: May not exceed 8.0 with or without

treatment.

Driving History: No more than 4 moving violations in

last 3 years. No DWI, DUI, reckless/negligent driving,

license revocation or suspension in the last 2 years.

Family History: No cardiovascular death of more than

one parent before age 60.

CAD- coronary artery disease is disregarded for applicants over

age 70 who don’t use tobacco.

Impairments: Can have personal history of certain

diseases or impairments.

Residency/Citizenship: U.S. citizen or legal permanent resident/green card

residing in the U.S. at least 2 years.

Substance/Alcohol Abuse: No abuse in past 7 years.

Tobacco Use: No use of tobacco or nicotine-based

products in last 12 months. One cigar allowed per month with HO specimen

negative for cotinine (for Standard Non-Tobacco.

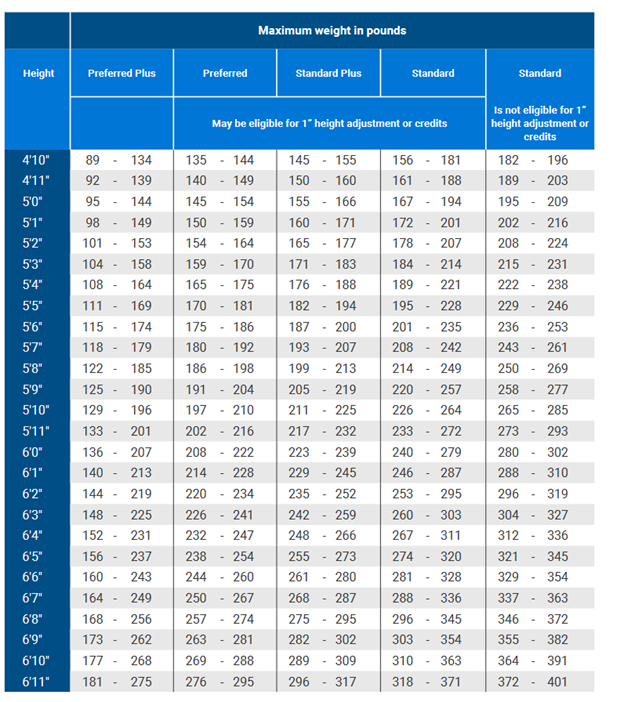

Banner Life Insurance Height & Weight Guidelines Build Chart: Preferred Plus, Preferred, Standard Plus, Standard

Minimum & maximum weight for each health class for Banner Life.

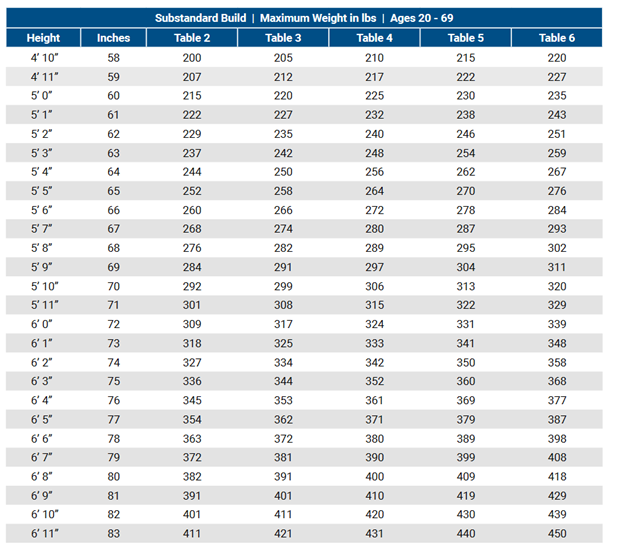

Banner Life Insurance Company Table Rates For Height & Weight Chart

Maximum weight for each table rate health class for Banner Life.

Large Cases- Jumbo Limits

| Ages | Amounts |

|---|---|

| 20-75 | $65 million |

| 76-85 | $30 million |

How Much Life Insurance Are You Eligible For?

Banner Life has one of the most favorable income limits for life insurance.

| Age | Multiple Earned Income by up to |

|---|---|

| Under 30 | 40X |

| 30-39 | 30x |

| 40-49 | 20x |

| 50-59 | 15x |

| 60-69 | 10x |

| 65-70 | 5x |

| 71+ | Individual consideration |

Banner Life & Large Policies: $5 Million – $65 Million

Banner does often like to write large cases. Their guidelines even state that large applications greater than $5 million face amount get all the special attention we know they require. Their underwriting professionals have the expertise necessary to drive these critically important cases through to policy issue. Their dedicated large case underwriters consult with professionals throughout their organization to ensure the

optimal decision is reached.

Banner Term Life Insurance Products

- 10 Year Term

- 15 Year Term

- 20 Year Term

- 25 Year Term

- 30 Year Term

- 35 Year Term

- 40 Year Term

Banner Life is one of only two life insurance companies in the nation that offer a 40-year level term policy. Protective Life is the other company. Also, there are only five life insurance companies in America that offer a 35-year level term.

Banner Life Insurance Company Health Classes

- Preferred Plus

- Preferred

- Standard Plus

- Standard

- Table 1

- Table 2

- Table 3

- Table 4

- Table 5

- Table 6

- Table 7

- Table 8

- Table 9

- Table 10

- Table 11

- Table 12

Banner Life often has the best table rates (substandard rates) in the nation. The reason why is that Banner uses the standard plus health class, then the table rate versus the other life insurance companies that use the standard health class, then the table rate. Also, see the table rates build chart above, Banner Life will often have the best rates for substandard height & weight.

Banner Term Life Insurance Rates By Age Chart-Male

| Age | $100k | $250k | $500k | $750k | $1 Million |

|---|---|---|---|---|---|

| 25 | $9 | $12 | $19 | $26 | $30 |

| 30 | $9 | $12 | $19 | $26 | $34 |

| 35 | $9 | $14 | $21 | $29 | $36 |

| 40 | $11 | $18 | $30 | $42 | $53 |

| 45 | $16 | $26 | $46 | $67 | $86 |

| 50 | $22 | $39 | $71 | $103 | $132 |

| 55 | $34 | $61 | $114 | $169 | $221 |

| 60 | $52 | $110 | $204 | $304 | $406 |

| 65 | $97 | $197 | $385 | $575 | $743 |

| 70 | $202 | $407 | $790 | $1,183 | $1,519 |

*The monthly rates are based on a male, at the preferred plus rate class for a 20-year level term.

Banner Term Life Insurance Rates By Age Chart-Female

| Age | $100k | $250k | $500k | $750k | $1 Million |

|---|---|---|---|---|---|

| 25 | $8 | $11 | $16 | $20 | $23 |

| 30 | $8 | $11 | $16 | $21 | $25 |

| 35 | $9 | $12 | $17 | $24 | $30 |

| 40 | $10 | $15 | $24 | $34 | $43 |

| 45 | $13 | $21 | $36 | $52 | $67 |

| 50 | $18 | $31 | $55 | $81 | $102 |

| 55 | $24 | $45 | $84 | $124 | $158 |

| 60 | $37 | $75 | $142 | $211 | $268 |

| 65 | $78 | $164 | $328 | $490 | $601 |

| 70 | $168 | $362 | $697 | $1,044 | $1,206 |

*The monthly rates are based on a female, at the preferred plus rate class for a 20-year level term.

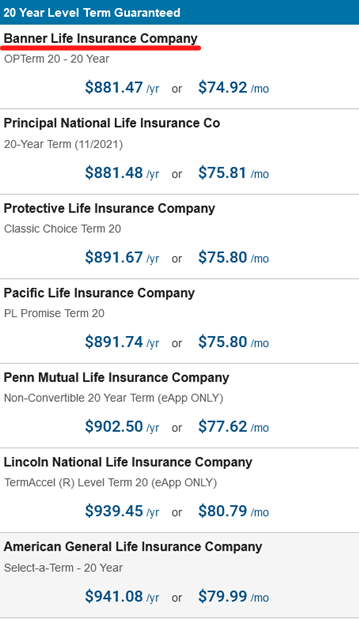

Banner Term Life Rates Comparison vs Competitors 2024

Banner Life’s term life insurance rates are often in the top 5 of all life insurance companies, many times they will have the lowest rate in the entire country (as seen in the graphic below) in 2024.

The quote example above shows the rates for a 50-year female (D.O.B. 12/15/1972) at the Preferred Plus health class for a $250,000 20-year level term from the best rates in the country from many of the top life insurers: Banner Life vs. Principal vs. Protective Life vs. Pacific Life vs. Sytmetra Life vs. AIG (American General).

Banner Life Insurance For Business

Key Person Life Insurance

| Ages < 64 | Up to 10x applicant’s annual income (salary & bonus) |

| Ages 65-70 | Up to 5x applicant’s annual income (salary & bonus) |

| Ages >71 | Individual consideration |

Buy/Sell, Partnership, Stock Redemption Coverage

Coverage is determined by the percentage of ownership held by the applicant multiplied by the market value of the company.

Business Loans

- Typically for collateral assignment loans such as an SBA loan, Banner will cover up to 100% of the loan amount.

- Uncollateralized loans. Banner generally considers up to 80% of the loan amount

Banner Life Insurance Underwriting Case Studies

Case Study #1

A 55 year old male, looking for a $500k term policy for a 15 year term to protect his wife until retirement age as well as cover the mortgage until it’s paid off. He is 5’11” 220 lbs, was diagnosed with type II diabetes at age 51 and currently takes metformin. He also takes a blood pressure and cholesterol medication, both well-controlled. He sees his physician every year for a physical. His last A1c was 6.5. He was approved at standard plus health class with Banner. His rate for $500k 15 year level term was $141.01 month or $1,658.89 a year.

Case Study #2

A 67 year old male, seeking a $250k 10 year term policy to cover the mortgage and his spouse. His current policy is about to expire. He is 6’2” 210 lbs. He was diagnosed with prostate cancer four years ago and had a radical prostatectomy. He has a checkup every year with his doctor and his last PSA was negligible. He is taking a blood pressure medication which is controlled on the medication. He was approved at standard plus health class with Banner. His rate for $250k 10 year term was $188.00 month or $2,211.74 a year.

Case Study #3

A 44 year old female is starting her own medical practice and needed $1 million life insurance policy to cover the SBA Loan requirement. She is healthy, 5’6” 140 lbs and taking Synthroid (levothyroxine) for hypothyroidism. She was approved at the best health class with Banner, Preferred Plus. $1 million on a 10 year term was $42.33 month or $497.99 a year.

Banner Life Insurance Review 2024- Final Thoughts

Banner Life is the largest provider of term life insurance in United States with $63 billion of new term life insurance issued in 2021. Banner became the top provider of term life insurance in the country by offering some of the absolute lowest term rates for healthy people and also specializing in certain niches such as diabetes. One of the secrets to Banners success is the fact that they do not not advertise like more well-known insurers which allows them to pass that savings to their customers.

Not only does Banner Life have often have the best term life insurance rates in the nation, they are also one of the highest rated life insurance companies as well. Banner is Superior rated (the highest category) which is the same financial rating category as other well-known insurers such as State Farm, New York Life, Northwestern Mutual, MassMutual, Prudential and USAA.

With Banner Life’s parent company being Legal & General, one of the largest insurance companies in the world, dating back to 1836 and Banner Life with an A+ (Superior) financial rating, a 95 Comdex score and having never failed to pay out a valid claim, you can’t go wrong with selecting Banner Life Insurance as your life insurance provider to protect your family.

FAQs

Is Banner Life Insurance A Good Company?

Does Banner Life Insurance Offer Whole Life Insurance?

Is Banner Life Insurance Good For Diabetics?

How Do I Get Instant Banner Term Life Insurance Quotes?

Does Banner Life Insurance Company Required a Medical Exam?

Instant Banner Life Insurance Quotes: $100k to $10 Million – 10 Year Term, 15 Year Term, 20 Year Term, 25 Year Term, 30 Year Term, 35 Year Term, 40 Year Term

1. Banner- About Us Financial Strength