20-Year Term Life Insurance Guide 2024

Posted in Term Life Insurance last updated on August 31, 2024

Posted in Term Life Insurance last updated on August 31, 2024Estimated reading time: 7 minutes

If you’re searching to learn more about a 20-year level term life insurance policy then you’ve come to the right place. In this article, we’ll show you the best rates in the country for a 20-year level term life insurance policy as well as how to to purchase the policy and alternatives.

Table of contents

- What Is A 20-Year Term Life Insurance Policy?

- How Does A 20-Year Term Life Insurance Policy Work?

- How Much Does A 20-Year Term Life Insurance Policy Cost for A Female?

- How Much Does A 20-Year Term Life Insurance Policy Cost for A Male?

- 20-Year Term Life Insurance Rates Illustration

- What Is The Cost for A 20-Year Term Life Insurance Policy With No Medical Exam?

- Alternatives To A 20-Year Term Life Insurance Policies

- Best Life Insurance Companies for A 20-Year Level Term Life Insurance Policy

- 5 Frequently Asked Questions (FAQ) 20-Year Term

What Is A 20-Year Term Life Insurance Policy?

A 20-year term level life insurance policy very straightforward. It means:

- The rates are fixed for 20 years

- The coverage amount is fixed for 20 years

- The rate cannot increase for 20 years

- Cancel during the 20 years anytime without a penalty

How Does A 20-Year Term Life Insurance Policy Work?

The way a 20-year level term life insurance policy works is:

- The insured pays the monthly or annual premiums and if they die during the term, the policy face amount is paid to the beneficiaries.

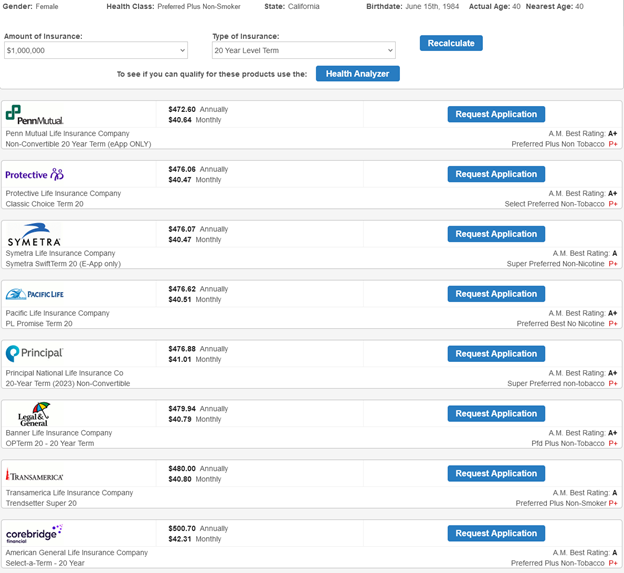

How Much Does A 20-Year Term Life Insurance Policy Cost for A Female?

Below is a 20 year term life insurance rate chart that shows the lowest monthly premiums in the country for a 20-year level term life insurance policy for $500k, $1 million and $2 million for a 40-year old female in excellent health.

Insurer | $500k | $1 Million | $2 Million |

|---|---|---|---|

$24.23 | $40.64 | $75.27 | |

$23.94 | $40.79 | $78.54 | |

$23.94 | $40.47 | $75.57 | |

$23.95 | $40.47 | $74.69 | |

$24.00 | $40.51 | $75.93 | |

$24.29 | $41.01 | $75.57 |

*Rates for a 40-year old female, in excellent health for a 20-year level term life insurance policy.

*Rates for Penn Mutual and Principal are for their Non-Convertible term life policy, policy does include accelerated death benefit rider at no-cost. All other companies include are convertible and include an accelerated death benefit rider at no-cost.

How Much Does A 20-Year Term Life Insurance Policy Cost for A Male?

The chart below shows lowest monthly rates in the country for a 20-year level term life insurance policy for $500k, $1 million and $2 million for a 40-year old male in excellent health.

Insurer | $500k | $1 Million | $2 Million |

|---|---|---|---|

$28.39 | $48.76 | $91.50 | |

$29.75 | $52.70 | $100.01 | |

$28.39 | $48.74 | $91.96 | |

$28.39 | $48.74 | $91.18 | |

$28.42 | $49.00 | $92.90 | |

$28.75 | $49.36 | $92.96 |

*Rates for a 40-year old female, in excellent health for a 20-year level term life insurance policy.

*Rates for Penn Mutual and Principal are for their Non-Convertible term life policy, policy does include accelerated death benefit rider at no-cost. All other companies include are convertible and include an accelerated death benefit rider at no-cost.

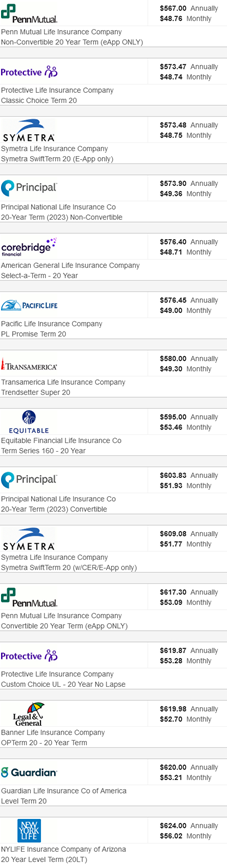

20-Year Term Life Insurance Rates Illustration

Below is an illustration of the of the of lowest rates in the country for a 20-year term life insurance policy for $1,000,000 coverage amount for ten of nation’s best term life companies: Penn Mutual, Protective Life, Symetra Life, Principal National, Corebridge Financial, Pacific Life, Transamerica, Equitable Financial, Banner Life, Guardian Life and New York Life.

*Rates for a $1,000 20-year term life insurance policy for a 40-year old male in excellent health

What Is The Cost for A 20-Year Term Life Insurance Policy With No Medical Exam?

Below are the monthly rates for no-exam 20-year level term life insurance policy for applicants 20-60 years old in excellent health for $500k, $1 million and $2 million in coverage.

Age | $500k | $1 Million | $2 Million |

|---|---|---|---|

30-Year Old Female | $15 | $23 | $40 |

30-Year Old Male | $18 | $29 | $53 |

40-Year Old Female | $24 | $40 | $74 |

40-Year Old Male | $28 | $48 | $91 |

50-Year Old Female | $54 | $95 | $184 |

50-Year Old Male | $69 | $129 | $251 |

60-Year Old Female | $126 | $242 | $479 |

60-Year Old Male | $200 | $381 | $756 |

*Rates for 20-year term life policies show above are convertible and have an accelerated death benefit rider both include at no additional cost.

Alternatives To A 20-Year Term Life Insurance Policies

Below are the most common alternatives for a 20-year term life insurance policy:

- 10-Year Term

- 15-Year Term

- 25-Year Term

- 30-Year Term

- Guarantee Universal Life Insurance (GUL)

Best Life Insurance Companies for A 20-Year Level Term Life Insurance Policy

Below are some of the best 20-year term life insurance companies in the country for; healthy, seniors, diabetics and no-exam applicants.

- Healthy: Pacific Life, Penn Mutual, Banner Life, Protective Life, Symetra Life, Corebride, Principal

- Older People: Pacific Life, Banner Life, Protective Life, Symetra Life, Penn Mutual, Transamerica, Foresters

- Diabetics: Banner Life, Pacific Life, Corebridge, John Hancock, Prudential

- No-Exam: Symetra Life, Banner Life, Pacific Life, Brighthouse, Corebridge, Penn Mutual, SBLI

Steps To Secure A 20-Year Term Life Insurance Policy

- Compare Quotes:

The first step is to receive quotes. With several hundred term life insurance companies in America, it’s important to narrow down which insurer will have the best rates based on the applicants age, health, family history, medications and height & weight. One can call several life insurance companies individually to receive and compare rate quotes or use a life insurance broker who can do the shopping for the applicant. (There is no charge to use a broker)

- Apply

When the applicant finds the best company for their 20-year term policy, the second next step is to apply and complete the insurance application. This is completed online or over the phone depending on the company.

- Underwriting

Once the 20-year term life insurance application has been submitted, the third step is underwriting. The life insurance company will let the applicant know if they are eligible for a no-exam application or if a 30-minute no-cost medical exam will be required. If medical records are requested by the underwriter, the applicant will have to wait until those are received.

- Approval & Activation

Once the policy is underwritten and approved, the fourth step is to decide on the final coverage amount and if accepted, make a payment then activate the 20-year policy.

5 Frequently Asked Questions (FAQ) 20-Year Term

When a 20-year term life insurance policy expires, most companies allow the insured to keep the policy but at a MUCH higher premium. For those under 70 years of age, many policies will provide the option to covert a portion or the full policy amount to permanent coverage.

A 20-year term life insurance policy is for anyone that needs financial protection for a loved one for a twenty year period. This typically includes those looking to protect a spouse until retirement age, children until they are adults or a mortgage until it’s paid off.

To be eligible for a 20-year term life insurance policy an applicant much be between the ages of 18-70 years old. At 71, a 20-year term policy is no longer available.

A 20-year term life insurance calculator can be found here. This calculator will show the rates, ratings and policy names from the largest term life insurance companies that offer a 20-year term.

There are four selections that need to be made when buying a 20-year term life insurance policy? 1. Selecting the insurance company. 2. Selecting the coverage amount. 3. Naming the beneficiary, beneficiaries and optional is adding contingent beneficiaries. 4. Choosing the payment mode, monthly is the most common and will require an EFT that automatically drafts the payments from a checking account. Additional payment options include quarterly, semi-annual or annually which can also be EFT or be direct bill (online payment).

Keep Reading:

- $1 Million Life Insurance Policy-Rates by Age

- $2 Million Life Insurance Policy

- Average Cost of Term Life Insurance Rates by Age Chart

- 10 Year Term Life Insurance Policy

- 10 vs 15 vs 20 vs 25 vs 30 Year Term Life Insurance

- A+ Rated Life Insurance Companies

- Best Term Life Insurance Companies 2024

- Best No-Exam Term Life Insurance Companies 2024

- Pacific Life Insurance Company Review

- Primerica Life Insurance Rates by Age Chart

- AARP Term Life Insurance Rates by Age Chart

- Life Insurance Over 50 No Medical Exam- $50k-$3 Million