Corebridge Financial – AIG Life Insurance Review 2023

last updated on March 22, 2024

last updated on March 22, 2024Searching to see if Corebridge Financial (formerly AIG Life Insurance) is a good life insurance company?

We have worked with AIG Life Insurance (underwritten by American General Life Insurance Company) for more than a decade and can tell you everything you need to know about choosing them as your life insurance company.

AIG Life and Retirement completed a spin-off and rebranded as Corebridge Financial in September 2022, therefore this review will include both names since it is so recent.

In this Corebridge Financial – AIG Life Insurance review 2023, we will go over the rates, financial ratings, product details, underwriting, the fine print and pretty much everything else you need to know about Corebridge Financial (formally AIG Life Insurance) and their subsidiaries American General Life Insurance and AIG Direct – soon to be Corebridge Direct Life Insurance.

Article Quick Navigation

About: Corebridge Financial (formally AIG Life Insurance)

Founded: AIG’s domestic life insurance company (American General Life Insurance Company) was founded in 1850. In September 2022, AIG’s Life & Retirement business spun-off and was rebranded Corebridge Financial.

Website: corebridgefinancial.com

Phone: (800) 888-2452

AIG Direct (Corebridge Direct) Address: 9640 Granite Ridge Drive, Suite 200 San Diego, CA 92123

J.D. Power Ranking: 744

AIG Life Insurance Awards: AIG was named one of DiversityInc’s Top 50 Companies for diversity. AIG earned a score of 100 on Human Rights Camping’s Corporate Equity Index. AIG donated $27 million for charitable giving in 2022.

AIG Life Insurance Reviews BBB: A+ (AIG Direct – Corebridge Direct)

AIG Life Insurance (Corebridge Financial) Ratings

| Rating Agency | Strength Ratings |

| A.M. Best | A (Excellent) |

| Fitch | A+ (Strong) |

| Moody’s | A2 (Upper-medium) |

| S&P Global | A+ (Strong) |

| Comdex | 80 |

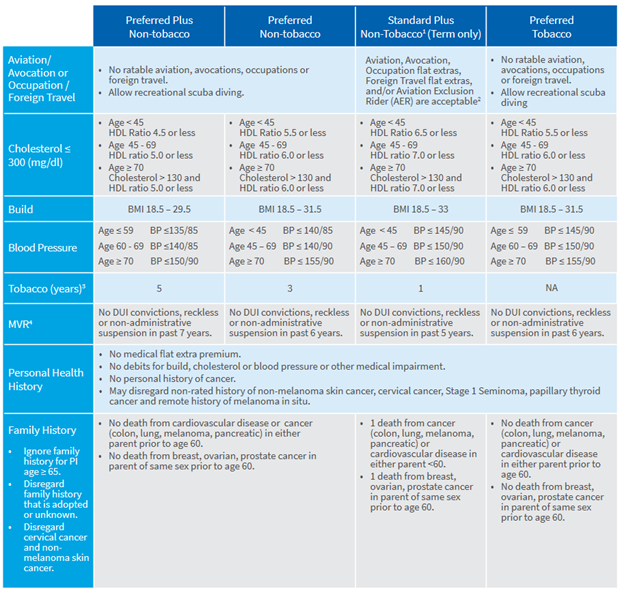

AIG Life Insurance Underwriting

Preferred Plus Health Class

AIG has very favorable underwriting in many areas that allow for the best health class as seen below:

- Cholesterol: Total cholesterol up to 300 with HDL ratio 4.5 or less, age 45-69 HDL ratio 5.0 or less

- BMI: 18.5 – 29.5

- Blood Pressure: Age ≤ 59 BP ≤135/85, Age 60 – 69 BP ≤140/85, Age ≥ 70 BP ≤150/90

- Driving Record: AIG has one of the most favorable DMV guidelines in the industry regarding tickets/violations. No DUI convictions, reckless or non-administrative suspension in past 7 years.

- Scuba Diving: Dives to depths not exceeding 100 feet and no more than 10 dives per year. No wreck, salvage, cave or under-ice diving.

- Family History: No deaths from either parent from cardiovascular disease (heart disease) or cancer (colon, lung, melanoma, pancreatic) prior to age 60. No death from breast, ovarian, prostate cancer in parent of same sex prior to age 60.

- Military: Very favorable guidelines for active military. Can have an alert or orders for overseas duty as long as not to a “hot spot”.

- Sleep Apnea: AIG has some of the most favorable sleep apnea guidelines, Preferred Plus eligible as long as not on a blood pressure medication.

- Anxiety/Depression: Application is eligible for Preferred Plus rate class if taking an anxiety or depression medication and controlled.

- H1B Visa: AIG is excellent for H1B visa holders.

- Cigar Smokers: AIG allows cigar users the best health class, non-smoker up to 52 cigars a year.

- Marijuana: Allowed to use marijuana 8 or less days per month may qualify for best class.

AIG Life Underwriting Guidelines By Health Class

AIG Underwriting Health Classes

- Preferred Plus (Pref. Plus)

- Preferred Non-tobacco (Pref. NT)

- Standard Plus (Std. Plus)

- Standard Non-tobacco (Std. NT)

- Substandard (Table Rates)

- Table A

- Table B

- Table C

- Table D

- Table E

- Table F

- Table G

- Table H

AIG Lab Scoring

AIG (American General) uses a lab scoring methodology to determine preferred rate classes and overall acceptability. Applicants with favorable lab scoring results, in addition to their established preferred criteria, are eligible to receive their best offers. The vast majority of applicants who previously met Preferred Plus, Preferred Non Tobacco, Standard Plus, or Preferred Tobacco rate class criteria continue to do so.

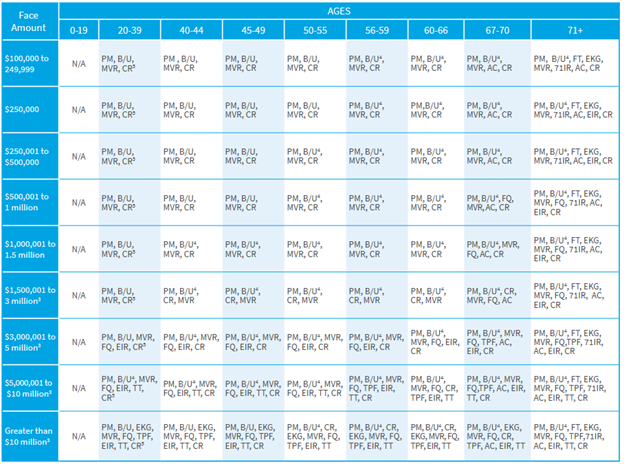

AIG Life Underwriting Requirements By Age & Amount For Term Insurance

- $100,000 to $249,999

- $250,000

- $250,001 to $500,000

- $500,001 to $1,000,000

- $1,000,001 to $1,500,000

- $1,500,001 to $3,000,000

- $3,000,001 to $5,000,000

- $5,000,001 to $10,000,000

- $10,000,001 +

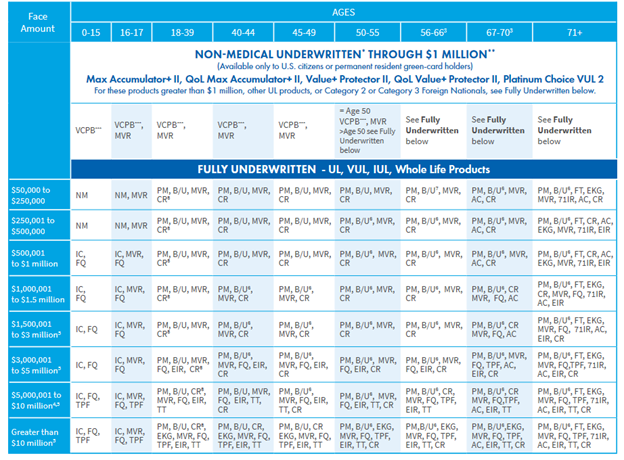

AIG Life Underwriting Requirements By Age & Amount For Permanent Insurance

- $100,000 to $249,999

- $250,000

- $250,001 to $500,000

- $500,001 to $1,000,000

- $1,000,001 to $1,500,000

- $1,500,001 to $3,000,000

- $3,000,001 to $5,000,000

- $5,000,001 to $10,000,000

- $10,000,001 +

AIG Life Insurance Height/Weight (BMI) Guidelines

AIG Life Insurance has very favorable height & weight (BMI) guidelines.

- Preferred Plus: BMI 18.5 – 29.5

- Preferred: BMI 18.5 – 31.5

- Standard Plus: BMI 18.5 – 33

Don’t know your BMI? Use this BMI calculator from the CDC here.

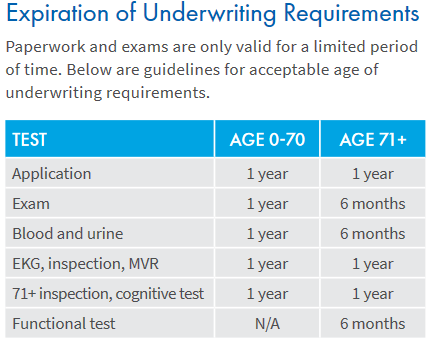

How Long Is The AIG Life Insurance Application & Paramed Exam Good For?

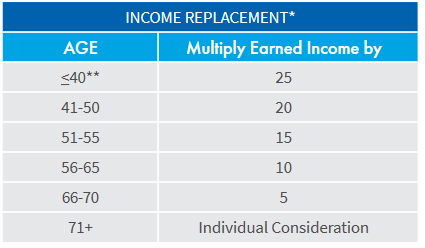

AIG Maximum Coverage Amount Available By Age & Income

Age Maximum Amount

<40 25 x annual income

41-50 20 x annual income

51-55 15 x annual income

56-65 10 x annual income

66-70 5 x annual income

71 and over Individual Consideration

Non-Working Spouse Age 59 or Less

- Can use household income to justify coverage through $1,500,000, using income replacement multiples. Amounts over $1,500,000 will be individually considered based on estate planning needs.

Non-Working Spouse, age 60-65

- If household income is less than $25,000, will allow up to 10 times the income of the working spouse.

Estate Conservation

- Need is based on the taxable value of the estate. Maximum allowable growth rate is 6 percent up to a maximum limit of double the current gross estate.

Key Person

- Maximum of 10 times total compensation. In some circumstances. In some circumstances, 3 to 5 times compensation will be considered as an appropriate maximum.

Buy-Sell/Business Succession/Business Continuation

- Coverage is limited to the market value of the proposed insured’s portion of the business as detailed in the Buy-Out or Buy-Sell agreement, or third party financials.

Business Loan Coverage

- Minimum 5 years remaining on the loan, coverage limited to 75 percent of loan, prorated per each owner’s percent share of the business. Business will be the owner and beneficiary with collateral assignment to the debtor. Venture capital is limited to 50 percent coverage, prorated as above.

AIG Term Life Insurance Product Details

AIG’s term life insurance is excellent for:

- Replace your lost income for your family’s financial well-being

- Pay off mortgage for family home

- Pay final funeral expenses

- Cover tuition for your children’s education

- SBA Loan life insurance requirement

- Key person coverage

- Divorce agreement

- Buy-sell agreement

Product Name: Select-a-Term

Term Lengths Available: 10, 15, 20, 25, 30 and 35 year level term.

More on AIG 35 year term life insurance

Prices: AIG often has some of the most competitive term life insurance rates in the country.

Minimum Amount: $100k ($100,000)

Conversion: AIG offers a conversion option to permanent insurance on their term product. Typically you can convert your term life insurance policy to a permanent life insurance policy with AIG up until age 70 or before the term ends, whichever comes first.

Accelerated Death Benefit Rider:

Free rider that allows the ability to accelerate a portion of the policy’s death benefit via the Accelerated Death Benefit Rider if you become terminally ill.

Additional Services:

•Choice of premium payment mode: annually, semi-annually, quarterly, or monthly

•Choice of electronic policy delivery for ease and convenience

.•Choice of electronic application for potentially faster turnaround times

AIG Term Life Insurance Product Brochure

AIG Term Life Life Insurance Rate Chart

| Age | $1 Million 10-Year Term | $1 Million 15-Year Term | $1 Million 20-Year Term | $1 Million 25-Year Term | $1 Million 30-Year Term | $1 Million 35-Year Term |

|---|---|---|---|---|---|---|

| 25 | $15 | $18 | $23 | $32 | $36 | $45 |

| 30 | $15 | $18 | $24 | $35 | $40 | $50 |

| 35 | $18 | $20 | $29 | $42 | $51 | $64 |

| 40 | $24 | $35 | $41 | $60 | $73 | $93 |

| 45 | $37 | $55 | $67 | $92 | $113 | $146 |

| 50 | $56 | $77 | $102 | $151 | $179 | NA |

| 55 | $90 | $113 | $162 | $260 | $332 | NA |

| 60 | $143 | $191 | $273 | $529 | NA | NA |

| 65 | $250 | $372 | $591 | NA | NA | NA |

| 70 | $387 | $597 | $1,325 | NA | NA | NA |

Rates for a female at the Preferred Plus health class, D.O.B. 12/15. Rates updated 12/23/2022

AIG Permanent Life Insurance Product (GUL) Details

AIG has one of the best no-lapse GUL policies in the country. It starts at $100k which makes it a great chose for final expenses in addition to estate planning.

- Estate planning

- Income replacement

- Final expenses

- Pass wealth to children, grandchildren or charitable organizations income tax free

- Guaranteed protection for life

- Debts that may last your lifetime such as a mortgage or a loan

- A special needs dependent

- Buy-sell agreement to have an orderly business succession

- Key person coverage

Product Name: Secure Lifetime GUL III (3)

No-Lapse Guarantee Protection Options To: Age 90, Age 95, Age 95, Age 100, Age 105, Age 110 or Age 121

Minimum Face Amount: $100k

Issue Ages: 18 to 80 years old

Diabetics: AIG has excellent underwriting for diabetics, especially on their guarantee universal life insurance policy.

Policy Coverage: Policy covers every type of death (except suicide in the first two years)

Waiting Period: None, covered from day one, once you are approved and make the first payment for their guaranteed universal life insurance product

Terminal Illness Rider Benefit: Included, no cost. Provides an accelerated death benefit (living benefit) when the insured is diagnosed with a terminal illness (12 months or less to live). One-time acceleration benefit of up to 50% of the base policy death benefit (less policy loans and excluding riders up to $250k.

Guaranteed Return of Premium: If your needs change or you no longer need life insurance coverage, you can surrender the policy in year 20 and receive 50 percent of premiums paid, or in year 25 and receive 100 percent of premiums paid up to 40% of face amount.

AIG Life Insurance Guarantee Universal Life (GUL) Product Brochure

AIG Universal Life Insurance Rate Chart

**Rates and policy amount are both fixed until age 121**

| Age | Male $100k | Female $100k | Male $1,000,000 | Female $1,000,000 |

|---|---|---|---|---|

| 25 | $64 | $59 | $409 | $368 |

| 30 | $76 | $74 | $515 | $459 |

| 35 | $89 | $75 | $637 | $553 |

| 40 | $114 | $102 | $775 | $672 |

| 45 | $131 | $117 | $937 | $811 |

| 50 | $144 | $132 | $1,069 | $985 |

| 55 | $158 | $151 | $1,356 | $1,207 |

| 60 | $197 | $174 | $1,647 | $1,394 |

| 65 | $264 | $224 | $2,196 | $1,825 |

| 70 | $394 | $331 | $3,141 | $2,760 |

| 75 | $540 | $500 | $4,635 | $4,093 |

| 80 | $904 | $672 | $7,828 | $6,416 |

Rates for a male and female at the Preferred Plus health class, D.O.B. 1/2. Rates updated 12/23/2022

AIG Direct (Corebridge Direct) Life Insurance Review 2023

When you purchase life insurance through AIG directly (now Corebridge Financial), you actually contact their call center which goes by the name AIG Direct (soon to be named Corebridge Direct), formerly called Matrix Direct which is based out of San Diego and was found in 1995. Matrix Direct was acquired by AIG in 2007. The primary insurance company that AIG Direct offers when you call in for a life insurance quote will of course be AIG (American General Life Insurance Company), their parent company.

What Life Insurance Companies Does AIG Direct Represent?

- American General Life Insurance Company

- Gerber Life Insurance Company

- Globe Life and Accident Insurance Company

- Prudential Life Insurance Companies

- Transamerica Life Insurance Companies

- Mutual of Omaha Insurance Company

Corebridge Financial (AIG) Life Insurance Review- Final Thoughts

AIG (American International Group) is a leading international insurance organization serving customers in more than 100 countries and jurisdictions and has more than 88 million customers worldwide. AIG is one of the most well-know brands in insurance, not only in America but the world.

AIG Life and Retirement completed a spin-off and rebranded as Corebridge Financial in September 2022, which is why you will see both names AIG and Corebridge.

Corebridge Financial (underwritten by American General Life Insurance Company) is also one of the best life insurance companies in America. AIG has very competitive rates for their term life insurance products, called Select-a-Term as well as their permanent life insurance policy, no-lapse guarantee universal life insurance called Secure Lifetime GUL III.

AIG has some of the best underwriting guidelines in certain areas such as sleep apnea, depression/anxiety treatment, H1B Visa holders, scuba divers, weekly cigar smokers, driving record and many other niches that make AIG the go to life insurance company for many of our clients. It is also important to note that AIG has has excellent underwriting for diabetics on their guarantee universal life insurance policy (GUL).

With an A (Excellent) financial rating from A.M. Best, a long history dating back to 1850, easy online payment and policy access, we recommend AIG to our clients when they have the best rate.

Frequently Asked Questions

Is AIG term life insurance good?

Yes, AIG (underwritten by American General Life Insurance Company) is one of the best term life insurance companies in the country.

Does AIG Life Insurance require a medical exam?

AIG’s (Corebridge Financial) term life insurance product called Select-a-Term, similar to other top insurers, allow some applicants who qualify to be to be eligible for accelerated underwriting. Factors such as age, health, coverage applying for, last physical exam with labs completed and other underwriting factors will determine if the 30-minute no-cost paramed exam is needed.

Is AIG Life Insurance (Corebridge Financial) & AIG Direct the same company?

Yes, AIG Direct is the call center for AIG Life Insurance (underwritten by American General Life Insurance Company). AIG Direct was formally known as Matrix Direct and was purchased by AIG to be their inside sales call center.

What is AIG life insurance payout rate?

100%. AIG life insurance has never failed to payout a valid claim.

What term lengths are available for AIG Life Insurance?

AIG offers: 10, 15, 20, 25, 30 and 35 year level term length options.

Does AIG Life Insurance (American General Life Insurance Company) have a good rating?

Yes, AIG Life Insurance (American General Life Insurance Company) has an A (Excellent) financial rating from A.M. Best.

How much is AIG life insurance?

The price for life insurance with AIG will depend on several factors such as your: age, coverage amount, policy length, medical history and several other factors. The best way to determine how much is AIG life insurance is to use our instant price quoter.

Where can I get an instant AIG Life Insurance quote?

You can receive instant AIG Life Insurance (Corebridge Financial) quotes here, as well as compare the rates from the other top life insurance companies.

What if I was declined/postponed by AIG Life Insurance due to Covid-19?

AIG Life Insurance (American General Life) had some of the most strict underwriting guidelines during the Covid-19 pandemic. If you were declined or postponed due to Covid, there are likely some other top insurers that will offer you coverage and at a good rate. However, this is does show that AIG (Corebridge Financial underwritten by American General Life) is a top life insurance company and protects their current and future policy holders.

Why PolicyMutual.com?

PolicyMutual.com not only represents Corebridge Financial (AIG) Life Insurance but also the other top 12+ life insurance companies. While AIG will have the best rate for some of our clients, they don’t always have the best rates for every client. Underwriting factors such as: coverage amount, policy length, age, height/weight, blood pressure, cholesterol, medical history and many other factors will determine which company will offer the best rate for your specific profile. That is why we recommend to compare rates from multiple top life insurance companies and choose the best one for you. The is no charge for our services, same price you receive by going though us is the same price if you go to the insurance company directly. If you have any questions don’t hesitate to get in contact with us.