How Much Life Insurance Should You Have? 2024

- 10x your gross annual income is the most common rule of thumb when determining the ideal amount of term life insurance coverage you should have

- Financial experts: Dave Ramsey recommends 10x to 12x your annual income in term life insurance coverage, Suze Orman recommends 20x to 25x your annual income in term life insurance coverage, Clark Howard recommends 10x your annual salary in term life insurance coverage

Are you looking to see how much life insurance you should have?

Great! You came to the right place.

In this article, we’ll show you how much life insurance you should have, the rule of thumb, as well as a show you a a more in-depth way to calculate your specific life insurance needs which will provide you the ideal amount life insurance you should carry to protect your family.

Table of contents

How Much Life Insurance Should You Have?

The amount of life insurance coverage you should have will depend on your age, needs, goals and budget.

Typically, the younger you are, the more life insurance coverage you should carry in relation to your annual income. This is due to the fact that if you were to suddenly pass away, you have more working years ahead of you and that income would need to be replaced to protect for you family.

Also, younger adults typically have a larger number of obligations to protect, such as dependent children, child care, newer mortgage, etc. compared to those who are over the age of 50, 60 or 70.

This is why Gen X, Millennials and Gen Z adults will typically need a higher multiple of their annual income in total personal life insurance coverage compared to Baby Boomers.

How Much Life Insurance Do I Need Rule of Thumb?

The general rule of thumb for life insurance is 5x – 20x your gross annual income (before taxes) in term life insurance coverage. Typically, the younger you are the more life insurance you will need in relation to the multiple of your annual income. This is because the younger you are, the more working years that are ahead and that income would need to be replaced in the event of a sudden death.

- Those between the ages of 21-60 typically need about 10x to 20x their annual income in term life insurance as a rule of thumb

- Seniors over the age of 60 looking to protect their income until retirement, often need about 5x to 10x their annual income in term life insurance coverage as a rule of thumb

Theoretically, a 35-year old that plans on retiring at age 65 has 30 more working years ahead of him or her. If they were to suddenly pass away, thirty years of income that would have been earned and used to provide for the family is now gone.

Life insurance is meant primarily for this reason, to replace current and future income that would be lost due to a premature death.

How Much Life Insurance Should You Have- Dave Ramsey?

Financial expert Dave Ramsey recommends 10x to 12x your annual gross income in term life insurance, as a rule of thumb. In fact, Mr. Ramsey is a very strong proponent of term life insurance compared to whole life insurance as seen in the video below.

Dave Ramsey states that the only job of life insurance is to replace your income when you die. It should not be used for anything else such as an investment vehicle.

How Much Insurance Should You Have- Suze Orman?

You may have seen the financial expert Suze Orman on her TV shows on CNBC, PBS or any number of other programs. Suze Orman recommends 20x to 25x your annual income in term life insurance as a rule of thumb, for most people.

Just like Dave Ramsey, Suze Orman recommends term life insurance unless someone in their family has special needs.

How Much Life Insurance Should You Have- Clark Howard?

Financial expert Clark Howard recommends 10 times your annual salary in term life insurance, as a rule of thumb. Just like Dave Ramsey and Suze Orman, Mr. Howard recommends “level term” life insurance for almost everyone. Level term life insurance means the premium and coverage amount are fixed for the term initially selected for the policy.

How Much Life Insurance Should You Have- Calculator

While the life insurance rule of thumb method is a great way to quickly and easily calculate how much life insurance you need to protect your loved ones, a life insurance needs calculator is an even more precise and personalized way to figure out how much life insurance is recommended to adequately protect your family if you were to unexpectedly pass away.

Life Insurance Needs Calculator

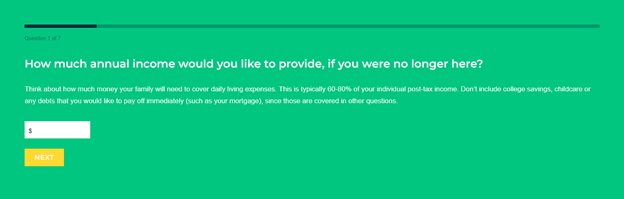

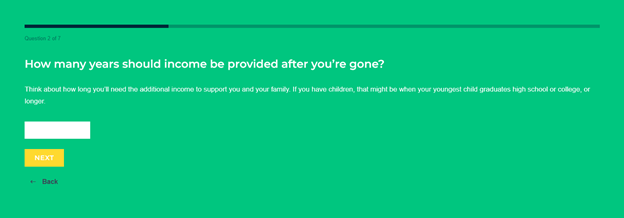

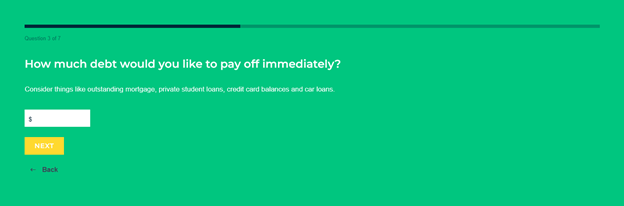

Below are the questions from the life insurance needs calculator from LifeHappens.org to help you determine the proper amount of life insurance you should have to protect your family.

- How much annual income would you like to provide, if you were no longer here?

- How many years should income be provided after you’re gone?

- How much debt would you like to pay off immediately?

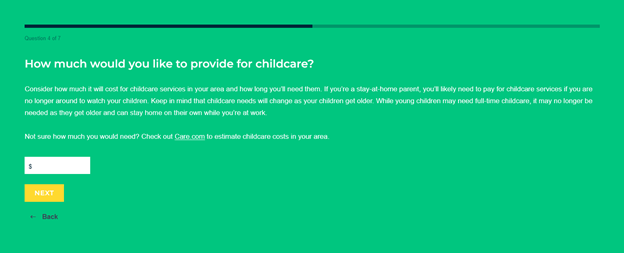

- How much would you like to provide for childcare?

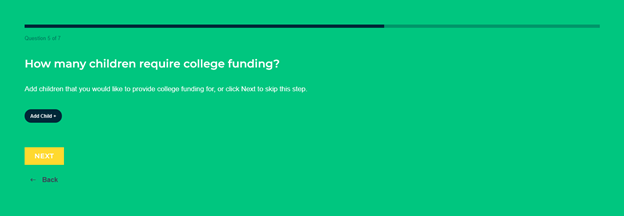

- How many children require college funding?

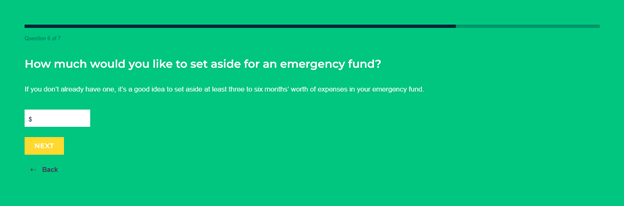

- How much would you like to set aside for an emergency fund?

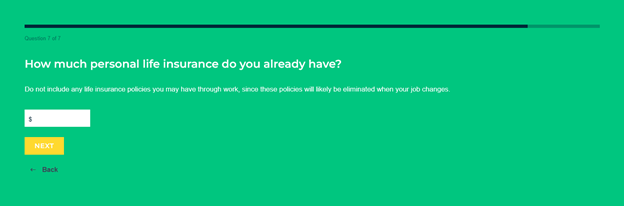

- How much personal life insurance do you already have?

- Your estimated life insurance need

1. Think about how much money your family will need to cover daily living expenses. This is typically 60-80% of your individual post-tax income. Don’t include college savings, childcare or any debts that you would like to pay off immediately (such as your mortgage), since those are covered in other questions.

2. Think about how long you’ll need the additional income to support you and your family. If you have children, that might be when your youngest child graduates high school or college, or longer.

3. Consider things like outstanding mortgage, private student loans, credit card balances and car.

4. Consider how much it will cost for childcare services in your area and how long you’ll need them. If you’re a stay-at-home parent, you’ll likely need to pay for childcare services if you are no longer around to watch your children. Keep in mind that childcare needs will change as your children get older. While young children may need full-time childcare, it may no longer be needed as they get older and can stay home on their own while you’re at work.

5. Add children that you would like to provide college funding for, or click Next to skip this step.

6. If you don’t already have one, it’s a good idea to set aside at least three to six months’ worth of expenses in your emergency fund.

7. Do not include any life insurance policies you may have through work, since these policies will likely be eliminated when your job changes.

8. Your total estimated life insurance need including: income replacement, debts to pay off, childcare, college fund, emergency fund, burial cost, minus current personal life insurance in force equals your total need.

The calculator above is from LifeHappnes.org. Life Happens is a nonprofit that provides unbiased information and tools to help people make smart decisions to protect their loved ones.

As you can see in the steps above, the life insurance needs calculator provides a great estimate on the amount of life insurance you should actually have to protect your loved ones. Not only does the calculator show the amount monetarily, it also makes you answer some tough questions and provides a real perspective the affect of a sudden loss would have on the ones left behind financially.

How Much Life Insurance Should You Have? Three Case Studies

Let’s take a look at several case studies to show much life insurance people chose to carry to protect their loved ones.

Case Study #1

A 30-year old male, has a wife a two year-old and his wife is pregnant with their second child. He makes $75k a year in annual income. He has a group life insurance policy from work for 1x his annual salary that goes away if he leaves his employer. He and his wife own a home with 28 years left on the mortgage at a balance of $380k. His wife currently works full-time and makes $50k a year. He choose a $750k 30-year level term policy. This is 10x his gross annual income in life insurance coverage. He chose this policy because if he were to prematurely pass away, the policy proceeds would: pay off the mortgage so the family can stay in their home and protect his wife children until the kids are out of college. His premium was $41 month since he was in excellent health.

He also received a quote for whole life insurance which would cost $300 month for the same $750k worth of coverage. He took Dave Ramsey, Suze Orman and Clark Howard’s advice and chose a term life insurance policy. He is going use that $250 + savings each month and put it in his own 401(k) every month and also use some of that savings to start contributing to a 529 plan for his children.

Case Study #2

A 43-year old female, is married and has two dependent children. She works full-time and makes $100,000 a year. Her husband also works and makes $80k a year. They have a $500k mortgage balance with 24 years left. She choose a $1 million 20-year level term policy for $54 month (she was in excellent health). This policy would pay off the mortgage, replace her income and protect her two children until they completed their higher education if anything were to happen to her in the next twenty years. Her and her husband also contribute substantially to their 401(k)s each year and make an extra payment or two on their mortgage each year.

Case Study #3

A 62-year old male, makes $120k a year and is looking to protect his wife, who does not currently work until his retirement. His children are grown and adults. He wants to be able to pay off the mortgage and replace his income should anything happen to him. His mortgage has 13 years left with a balance of $300k. They have substantial equity in the home and he plans on retiring before age 70. They also hope to have the mortgage paid off or nearly paid in the next ten years. There is a substantial balance amount in his 401k. He is eligible to receive social security at his current age, but doesn’t plan on taking it until age 67 or age 70.

He chose a $500k 15-year level term since it cost $203 month (preferred plus health class) for the peace of mind.

How Much Life Insurance Are You Eligible For?

Life insurance companies use a multiple of income factor to determine the total amount (maximum amount of coverage) of personal life insurance someone is eligible to have active. This does not include the group coverage offered through an employer. Life insurance companies use this formula to make sure the insured is worth more dead than they are alive. As previously noted, the younger you are the greater the multiple of your income in life insurance you are eligible for since there is more working years that would need to be replaced in the event of an unexpected death.

Below is a sample multiple of income table from one of the largest life insurance companies, Pacific Life.

| Age | Maximum Factor |

|---|---|

| 21-40 | 30 x annual income |

| 41-50 | 20 x annual income |

| 51-60 | 15 x annual income |

| 61-70 | 10 x annual income |

| 71 and over | 5x annual income or individual consideration |

Bottom Line

The amount of life insurance you should have will depend on your age, number of dependents, outstanding debts and your needs and goals. The answer to the question of “how much life insurance do I need rule of thumb” is typically between 5x to 25x your annual income in life insurance coverage. The average being 10x your annual gross income (before taxes) in personal (outside of work) life insurance coverage one should have active.

The younger you are the more working years that are ahead and that income would need to be replaced for your family should an unexpected death occur. This is why Gen X, Millennials and Gen Z will typically need more life insurance coverage in relation to their annual income compared to someone in their mid-to-late 50’s, 60’s or 70’s.

By using the life insurance rule of thumb life insurance need calculation method or more precisely using the life insurance needs calculator, you can be confident that you are loved ones will be properly taken care of should the unexpected occur.

FAQ

Is life insurance taxed?

No, life insurance payout proceeds are income tax free (unless subject to estate taxes).

How much life insurance should a stay-at-home parent have?

A stay-at-home parent typically carries half the life coverage of the working spouse. Although, most carriers allow a non-working spouse to match the same coverage amount the working spouse has.

The value that a stay-at-home parent contributes is often vastly underestimated, specifically in regards for life insurance. The costs to cover child care, taking time off to grieve, taking care of the house hold, etc. makes some amount life insurance coverage important for a stay-at-home parent. Securing a $100k, $250k or $500k or even $1 million for a 20-year term is the most common for the non-working spouse.

What if I can’t afford 10x my annual income in life insurance?

If you don’t have life insurance coverage, secure a life insurance policy now, any amount of life insurance if better than not having any life insurance at all. If you cannot purchase the ideal amount of life insurance per the calculator or by using the 10-12x annual income rule of thumb, most people can secure some amount of coverage today then purchase additional or the ideal amount life insurance at a later date (as long as they are healthy and qualify). Protect your family today!

Can you have multiple life insurance policies?

Yes, life insurance companies allow you to carry multiple life insurance policies. Life insurance companies use a multiple of income factor to determine the total amount of personal life insurance you can have active outside of your employer. For example, those between the ages of 21-40 are typically allowed to have 30x their annual income and those between the ages 41-50 are allowed to have 20x their annual income in personal (outside of work) life insurance.

Keep Reading

- 10 vs 15 vs 20 vs 25 vs 30 Year Term Life Insurance Policy

- Average cost of term life insurance: rates by age, term and amount

- Life Insurance Company Ratings 2024

- Best Life Insurance Companies That Pay Out 2024

- Life Insurance for SBA Loans (Ultimate Guide) 2024

- Banner Life Insurance Company Review

- Pacific Life Insurance Company Review

- $1 Million Life Insurance Policy- Best Rates by Age

- Best Rates for a $2 Million Life Insurance Policy Rates